Uganda’s declining foreign-currency lending is a credit positive for its banks as it will support their asset quality and reduce negative pressure on some banks’ foreign-currency funding and capital adequacy, says Moody’s Investor Service.

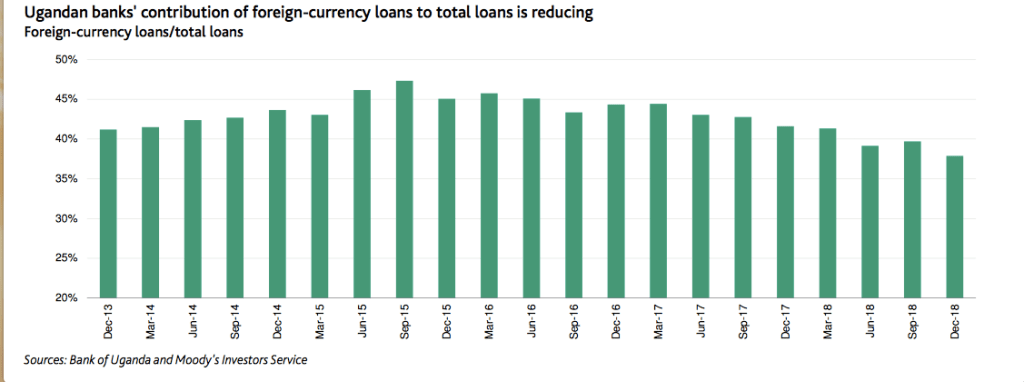

On 5 February, Bank of Uganda, the country’s central bank, released statistics showing that the ratio of foreign-currency loans to total loans declined to 37.9 per cent in 2018 from 41.6 per cent in 2017 and 44.3 per cent in 2016.

Ugandan banks’ foreign-currency loan volumes, predominantly in US dollars, contracted 1 per cent in 2018 when adjusted for the depreciation of the local currency, the Ugandan shilling, after declining 2 per cent in 2017.

Although the contraction erodes revenue from this income stream, banks are increasing their local-currency lending, supporting their lending fee income and interest income. In 2018, local- currency loans increased by 17 per cent, suppressing the proportion of foreign currency loans to 37.9 per cent, the lowest in the past five years.

Declining foreign-currency loans will ease asset risk because banks’ exposure to shilling depreciation will diminish. Between 2015 and 2018, the shilling-to-dollar exchange rate depreciated to UGX3,706 from UGX2,855, exposing banks’ unhedged clients to elevated default risk.

“We believe some foreign-currency loans were extended to borrowers whose revenue is in shillings, and a weaker shilling would require higher shilling cash flow for the borrowers to meet their foreign-currency loan repayments. The inability of such unhedged borrowers to increase prices when the shilling is weak erodes their operating margins and cash flow and diminishes their repayment capacity,” says Moody’s.

Although disclosure is limited, especially for smaller banks, foreign currency loans in 2017 contributed 43 per cent of total loans for Stanbic Bank Uganda Limited, the largest bank in the system, and 47 per cent of dfcu Group, the second-largest bank (the two banks’ combined market share by assets was about 32 per cent in 2017).

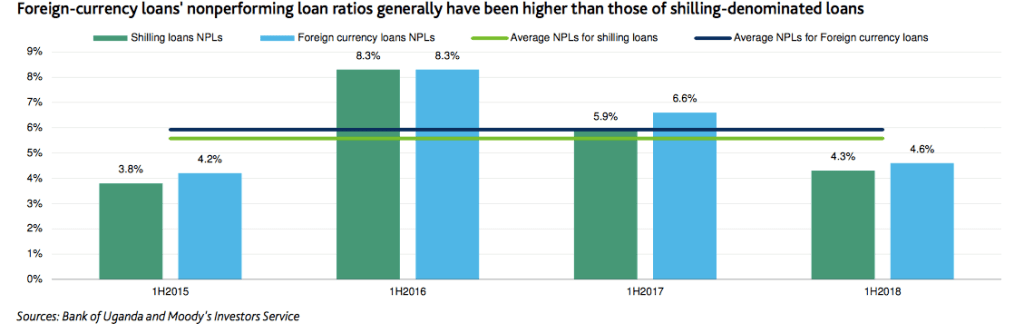

Defaults on foreign-currency loans have generally been higher than on local-currency loans, with a nonperforming loan ratio of 4.6 per cent in June 2018, versus 4.3 per cent for local-currency loans, and 6.6per cent in June 2017 versus 5.9 per cent for local-currency loans.

Fewer foreign-currency loans also will lessen foreign currency funding pressures for banks that depend on wholesale market funding to support their foreign currency assets. Uganda’s large current account deficit, at about 5 per cent of GDP, limits prospects of strong dollar deposit formation in the system, and any substantial foreign currency lending would require banks to rely on more expensive and confidence-sensitive market funds.

As of December 2017, dfcu Group’s proportion of foreign-currency loans to deposits was 109 per cent, creating a funding gap, while its local- currency loans-to-deposits ratio was only 50 per cent.

“We expect that the ratio declined to below 100% in 2018, removing the funding gap, as the bank cut back on foreign-currency lending and continued the downward trend from 116% in 2016,” sasys Moody’s.

For Stanbic, foreign- currency loans-to-deposits ratio is lower at 76 per cent, but remains higher than the 50 per cent for the local-currency portfolio. However, some of the market funds, especially from developmental financial institutions, are of long-term nature and they limit banks’ roll-over risk.

Ugandan banks’ capital adequacy ratios will also benefit from falling foreign currency loans because a weaker shilling inflates the banks’ risk weighted assets when the loans converts to a higher local-currency amount.

“We estimate that a 10% depreciation of the shilling would reduce capital adequacy ratio by about 90 basis points for banks with small open positions,” added Moody’s.

The shilling’s 12-month forward contract points to a weakening exchange rate of UGX3,981 per US dollar. Ugandan banks’ capital adequacy ratio will remain relatively solid. As of June 2018, the sector’s average ratio of regulatory capital to risk-weighted assets was 21.8 per cent