First Published on October 7th, 2022 by Bob Ciura for SureDividend

Investors looking to generate higher levels of income from their investment portfolios should take a look at Real Estate Investment Trusts, or REITs. These are companies that own real estate properties and lease them to tenants or invest in real estate backed loans, both of which generate a steady stream of income.

The bulk of their income is then passed on to shareholders, through dividends. You can see all 208 REITs here.

You can download our full list of REITs, along with important metrics such as dividend yields and market capitalizations, by clicking on the link below:

Click here to download your Complete REIT Excel Spreadsheet List now. Keep reading this article to learn more.

The beauty of REITs, for income investors, is that they are required to distribute 90% of their taxable income to shareholders annually, in the form of dividends. In return, REITs typically do not pay corporate taxes.

As a result, many of the 200+ REITs we track offer high dividend yields of 5%+.

But not all high-yielding stocks are automatic buys. Investors should carefully assess the fundamentals to ensure the high yields are sustainable.

Note that while the securities in this article have very high yields, a high yield alone does not make for a solid investment. Dividend safety, valuation, management, balance sheet health, and growth are all very important factors as well.

We urge investors to use the below analysis as informative, but to do significant due diligence before buying into any security – and especially high yield securities. Many (but not all) high yield securities have significant risk of a dividend reduction and/or deteriorating business results.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- •High-Yield REIT No. 10: PennyMac Mortgage Investment Trust (PMT)

- •High-Yield REIT No. 9: Apollo Commercial Real Estate Finance (ARI)

- •High-Yield REIT No. 8: Broadmark Realty Capital (BRMK)

- •High-Yield REIT No. 7: Office Properties Income Trust (OPI)

- •High-Yield REIT No. 6: New York Mortgage Trust (NYMT)

- •High-Yield REIT No. 5: AGNC Investment Corporation (AGNC)

- •High-Yield REIT No. 4: Two Harbors Investment Corp. (TWO)

- •High-Yield REIT No. 3: Annaly Capital Management (NLY)

- •High-Yield REIT No. 2: Chimera Inv. Corp. (CIM)

- •High-Yield REIT No. 1: ARMOUR Residential REIT (ARR)

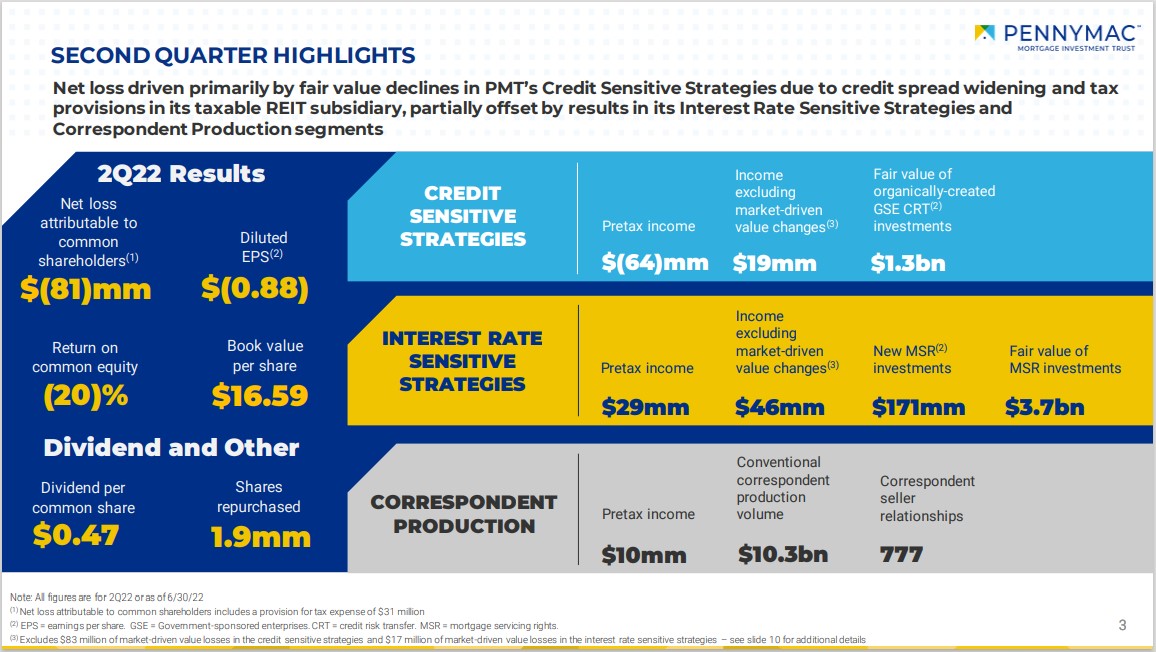

High-Yield REIT No. 10: PennyMac Mortgage Investment Trust (PMT)

- •Dividend Yield: 15.9%

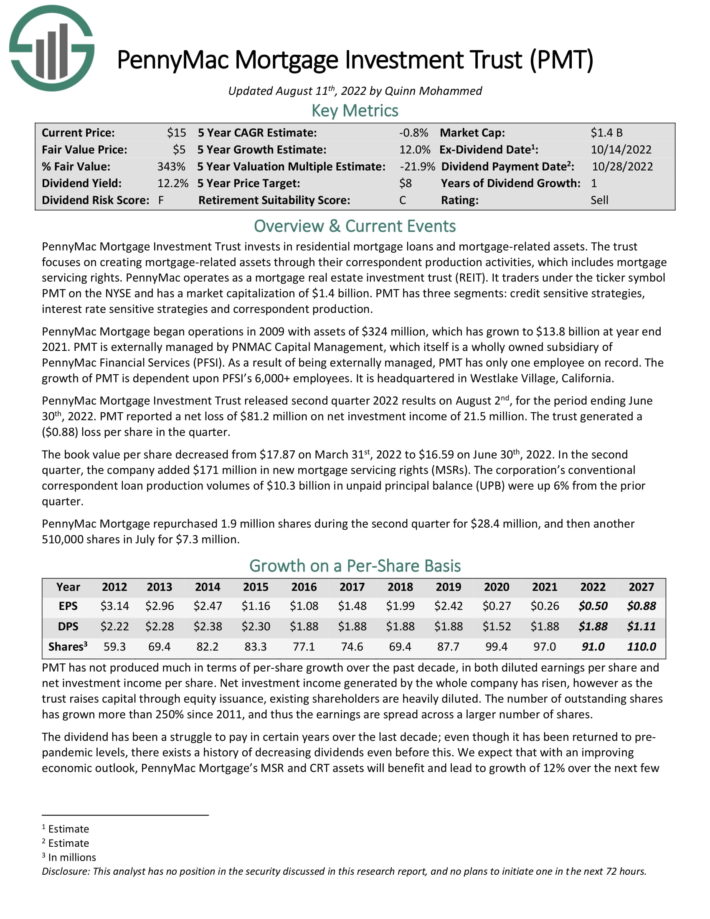

PennyMac Mortgage Investment Trust is a specialty REIT that invests in residential mortgage loans and mortgage-related assets. PMT is managed by PNMAC Capital Management, LLC, a subsidiary of PennyMac Financial Services, Inc. (PFSI).

Source: Investor Presentation

PMT believes it will generate long-term growth alongside a large (and growing) addressable market in its core industry.

PennyMac Mortgage Investment Trust released second quarter 2022 results on August 2nd, for the period ending June 30th, 2022. PMT reported a net loss of $81.2 million on net investment income of 21.5 million. The trust generated a ($0.88) loss per share in the quarter.

The book value per share decreased from $17.87 on March 31st, 2022 to $16.59 on June 30th, 2022. In the second quarter, the company added $171 million in new mortgage servicing rights (MSRs). The corporation’s conventional correspondent loan production volumes of $10.3 billion in unpaid principal balance (UPB) were up 6% from the prior quarter.

PennyMac Mortgage repurchased 1.9 million shares during the second quarter for $28.4 million, and then another 510,000 shares in July for $7.3 million.

Click here to download our most recent Sure Analysis report on PMT (preview of page 1 of 3 shown below):

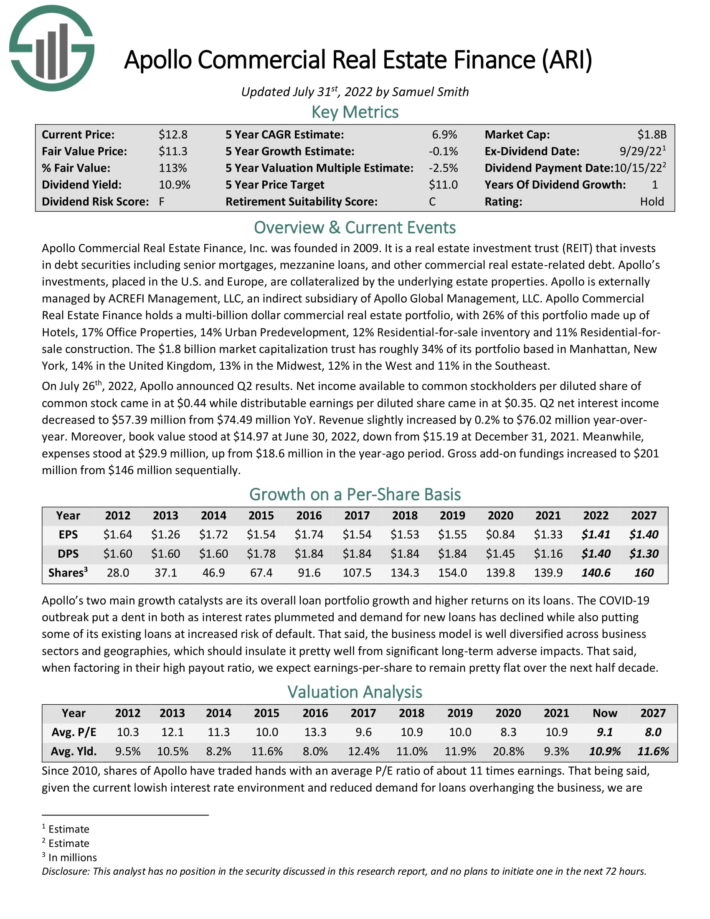

High-Yield REIT No. 9: Apollo Commercial Real Estate Finance (ARI)

- •Dividend Yield: 16.1%

Apollo Commercial Real Estate Finance invests in debt securities including senior mortgages, mezzanine loans, and other commercial real estate-related debt. Apollo’s investments, placed in the U.S. and Europe, are collateralized by the underlying estate properties. Apollo is externally managed by ACREFI Management, LLC, an indirect subsidiary of Apollo Global Management, LLC.

The trust has roughly 34% of its portfolio based in Manhattan, New York, 14% in the United Kingdom, 13% in the Midwest, 12% in the West and 11% in the Southeast.

Source: Investor Presentation

On July 26th, 2022, Apollo announced Q2 results. Net income available to common stockholders per diluted share of

common stock came in at $0.44 while distributable earnings per diluted share came in at $0.35. Q2 net interest income decreased to $57.39 million from $74.49 million YoY.

Revenue slightly increased by 0.2% to $76.02 million year-over-year. Moreover, book value stood at $14.97 at June 30, 2022, down from $15.19 at December 31, 2021. Meanwhile, expenses stood at $29.9 million, up from $18.6 million in the year-ago period. Gross add-on fundings increased to $201 million from $146 million sequentially.

Click here to download our most recent Sure Analysis report on ARI (preview of page 1 of 3 shown below):

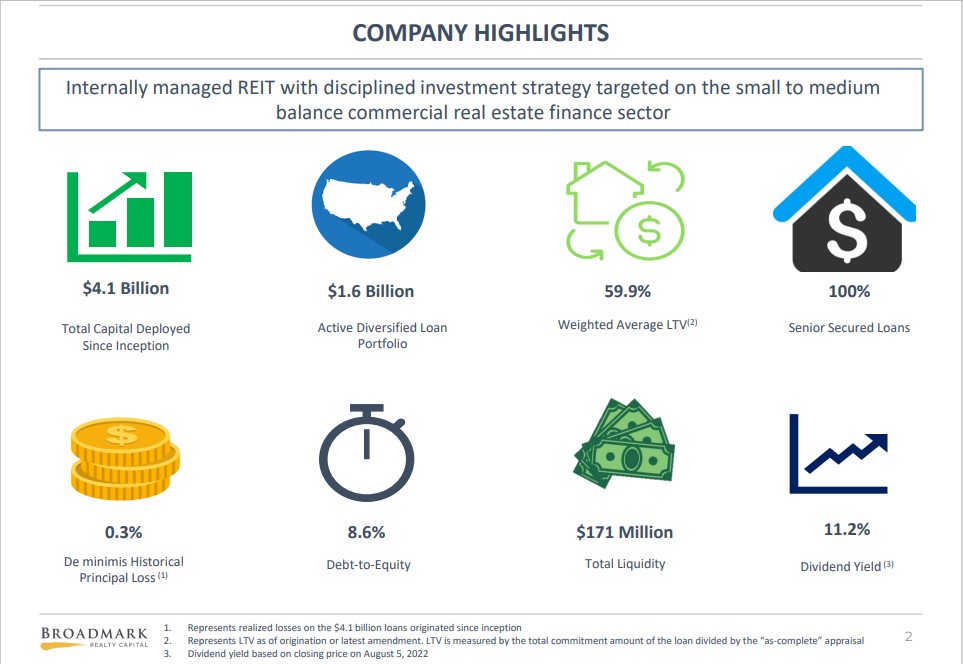

High-Yield REIT No. 8: Broadmark Realty Capital (BRMK)

- •Dividend Yield: 16.2%

Broadmark Realty Capital Inc. is a real estate investment trust that provides short-term, first deed of trust loans that are secured by real estate. Customers use these loans to acquire, renovate, rehab and develop properties for both residential and commercial uses in the U.S. Broadmark Realty formed in 2010, but had its initial public offering in November 2019.

Source: Investor Presentation

On August 9th, 2022, Broadmark Realty reported second quarter results for the period ending June 30th, 2022. For the quarter, revenue decreased 2.3% to $28.52 million, which was $1.48 million lower than expected. Adjusted earnings per share of $0.16 compared unfavorably to adjusted earnings per share of $0.18 in the prior period and was $0.01 below estimates.

Broadmark Realty originated $196.7 million of new loans and amendments for the quarter. Second quarter origination was a 3.7% increase sequentially and at a weighted average loan to value of 62%. Quarterly interest income totaled $22.1 million and fee income was $6.4 million. The total portfolio consisted of $1.6 billion of loans across 20 states and the District of Columbia.

As of June 30th, 2022, Broadmark Realty had a total of $91.7 million of loans in contractual default. Provisions for credit losses totaled $2.7 million compared to $58K in the second quarter of 2021.

Click here to download our most recent Sure Analysis report on BRMK (preview of page 1 of 3 shown below):

High-Yield REIT No. 7: Office Properties Income Trust (OPI)

- •Dividend Yield: 16.9%

Office Properties Income Trust owns 178 buildings, which are primarily leased to single tenants with high credit quality. The REIT’s portfolio currently has a 94.3% occupancy rate and an average building age of 17 years. The U.S. Government is the largest tenant of OPI, as it represents 20% of the annual rental income of the REIT.

Source: Investor Presentation

In late July, OPI reported (7/28/2022) financial results for the second quarter of fiscal 2022. The occupancy rate grew sequentially from 91.2% to 94.3% thanks to strong leasing activity and asset sales. Normalized funds from operations (FFO) per share grew 6% over the prior year’s quarter, from $1.15 to $1.22.

OPI generates 64% of its annual rental income from investment-grade tenants. This is one of the highest percentages of rent paid by investment-grade tenants in the REIT sector. Moreover, U.S. Government tenants generate about 20% of total rental income and no other tenant accounts for more than 4% of annual income. This exceptional credit profile constitutes a meaningful competitive advantage.

On the other hand, OPI has greatly increased its debt load after its latest acquisition. Its net debt is excessive, as it stands at $2.4 billion, which is about 11 times the annual funds from operations and 2.5 times as much as the current market capitalization of the REIT. Fortunately, OPI is in the process of selling assets and hence it is likely to drive its leverage to healthier levels in the near future.

Click here to download our most recent Sure Analysis report on OPI (preview of page 1 of 3 shown below):

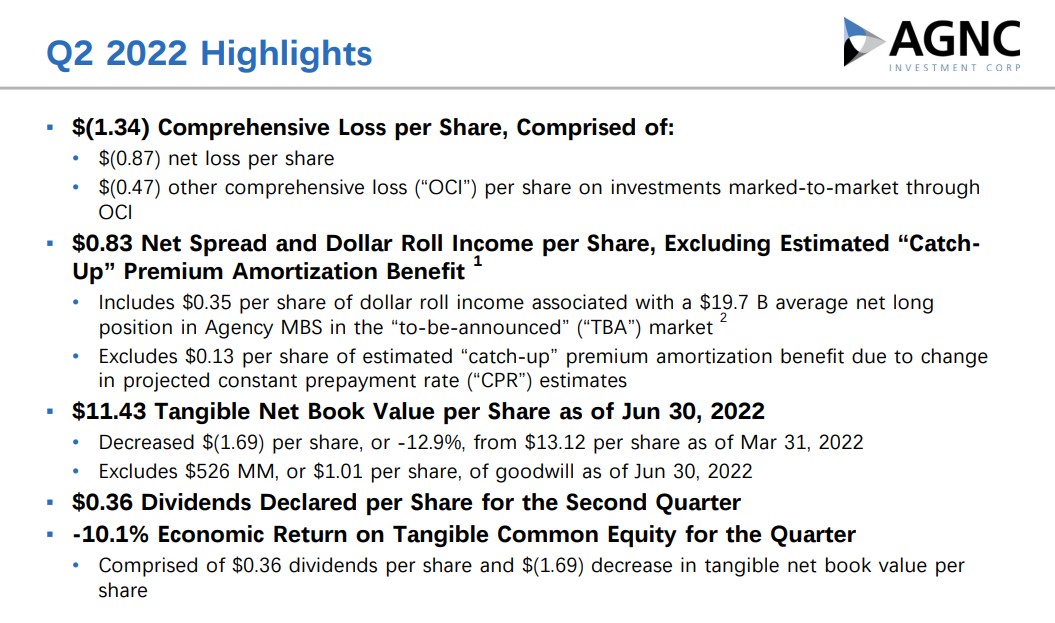

High-Yield REIT No. 5: AGNC Investment Corp. (AGNC)

- •Dividend Yield: 17.6%

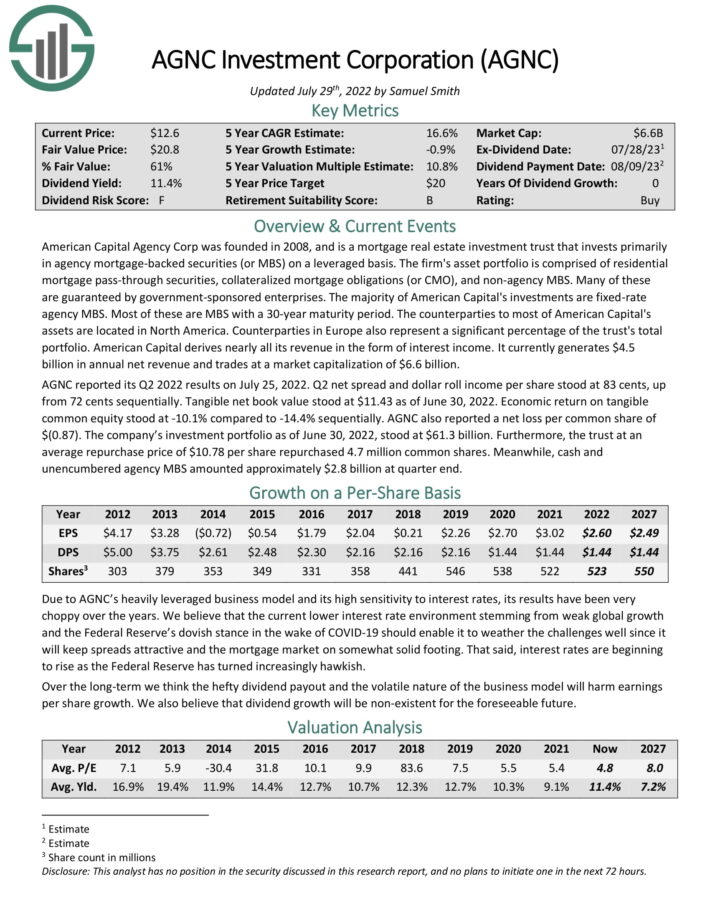

American Capital Agency Corp was founded in 2008, and is a mortgage real estate investment trust that invests primarily in agency mortgage-backedsecurities (or MBS) on a leveraged basis.

The firm’s asset portfolio is comprised of residential mortgage pass-throughsecurities, collateralized mortgage obligations (or CMO), and non-agencyMBS. Many of these are guaranteed by government sponsored enterprises.

The majority of American Capital’s investments are fixed rate agency MBS. Most of these are MBS with a 30-year maturity period. AGNC derives nearly all its revenue in the form of interest income. It currently generates $1.2 billion in annual net revenue.

You can see an overview of the company’s second-quarter report in the image below:

Source: Investor Presentation

AGNC reported its Q2 2022 results on July 25, 2022. Q2 net spread and dollar roll income per share stood at 83 cents, up from 72 cents sequentially. Tangible net book value stood at $11.43 as of June 30, 2022. Economic return on tangible common equity stood at -10.1% compared to -14.4% sequentially. AGNC also reported a net loss per common share of $(0.87). The company’s investment portfolio as of June 30, 2022, stood at $61.3 billion.

Furthermore, the trust at an average repurchase price of $10.78 per share repurchased 4.7 million common shares. Meanwhile, cash and unencumbered agency MBS amounted approximately $2.8 billion at quarter end

Click here to download our most recent Sure Analysis report on AGNC (preview of page 1 of 3 shown below):

High-Yield REIT No. 6: New York Mortgage Trust (NYMT)

- •Dividend Yield: 17.2%

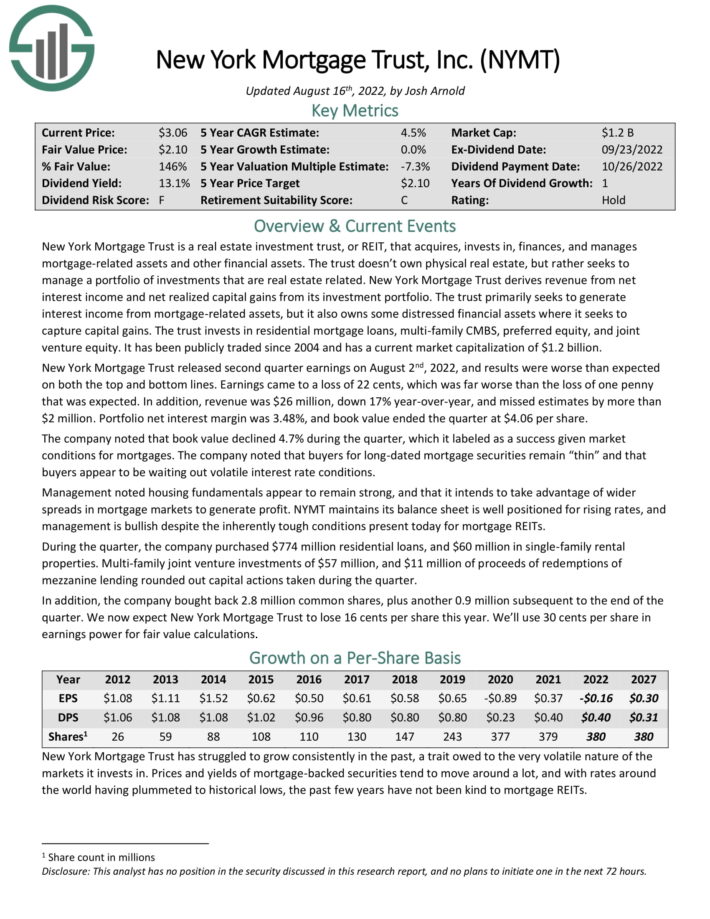

New York Mortgage Trust is a real estate investment trust, or REIT, that acquires, invests in, finances, and manages mortgage-related assets and other financial assets. The trust doesn’t own physical real estate, but rather seeks to manage a portfolio of investments that are real estate related. New York Mortgage Trust derives revenue from net interest income and net realized capital gains from its investment portfolio.

Source: Investor Presentation

The trust primarily seeks to generate interest income from mortgage-related assets, but it also owns some distressed financial assets where it seeks to capture capital gains. The trust invests in residential mortgage loans, multi-family CMBS, preferred equity, and joint venture equity.

Click here to download our most recent Sure Analysis report on NYMT (preview of page 1 of 3 shown below):

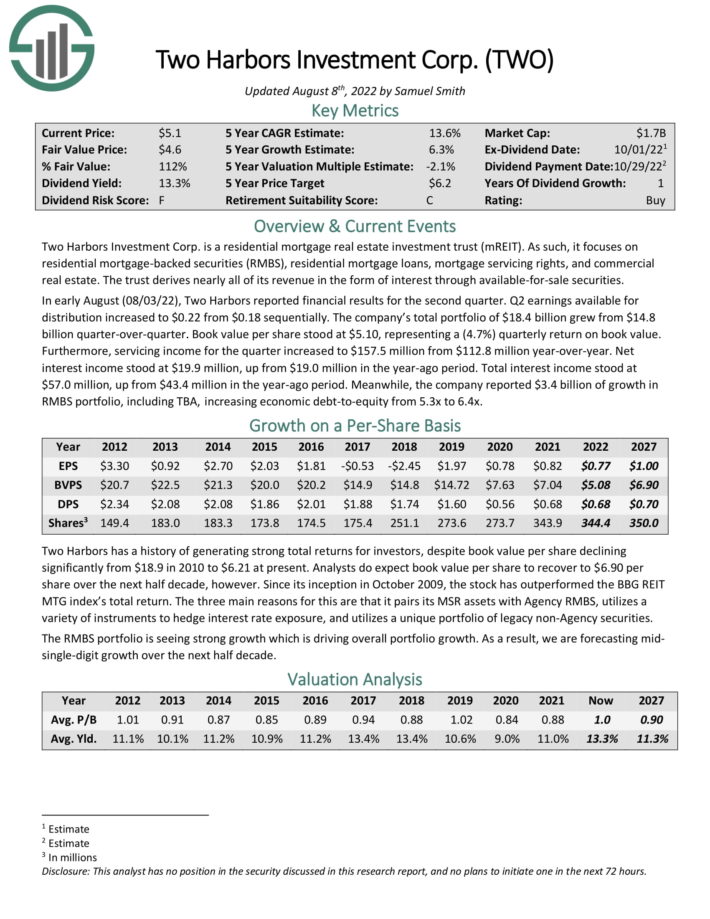

High-Yield REIT No. 4: Two Harbors Investment Corp. (TWO)

- •Dividend Yield: 20.4%

Two Harbors Investment Corp. is a residential mortgage real estate investment trust (mREIT). As such, it focuses on residential mortgage–backed securities (RMBS), residential mortgage loans, mortgage servicing rights, and commercial real estate.

The trust derives nearly all of its revenue in the form of interest through available–for–sale securities.

Source: Investor Presentation

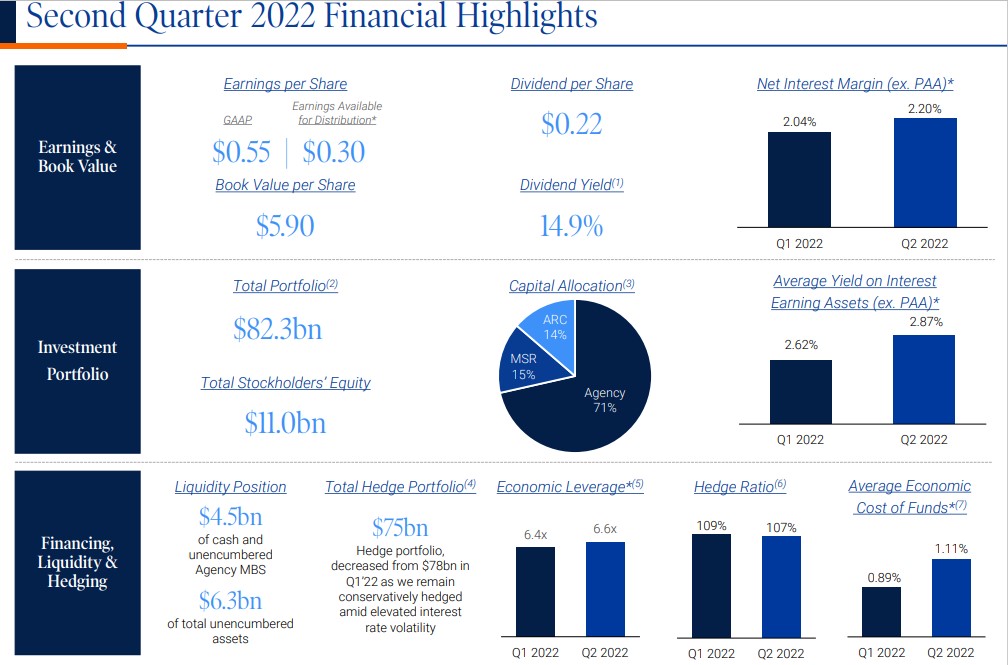

In early August (08/03/22), Two Harbors reported financial results for the second quarter. Q2 earnings available for distribution increased to $0.22 from $0.18 sequentially. The company’s total portfolio of $18.4 billion grew from $14.8 billion quarter-over-quarter. Book value per share stood at $5.10, representing a (4.7%) quarterly return on book value.

Furthermore, servicing income for the quarter increased to $157.5 million from $112.8 million year-over-year. Net interest income stood at $19.9 million, up from $19.0 million in the year-ago period. Total interest income stood at $57.0 million, up from $43.4 million in the year-ago period. Meanwhile, the company reported $3.4 billion of growth in RMBS portfolio, including TBA, increasing economic debt-to-equity from 5.3x to 6.4x.

Click here to download our most recent Sure Analysis report on Two Harbors (TWO) (preview of page 1 of 3 shown below).

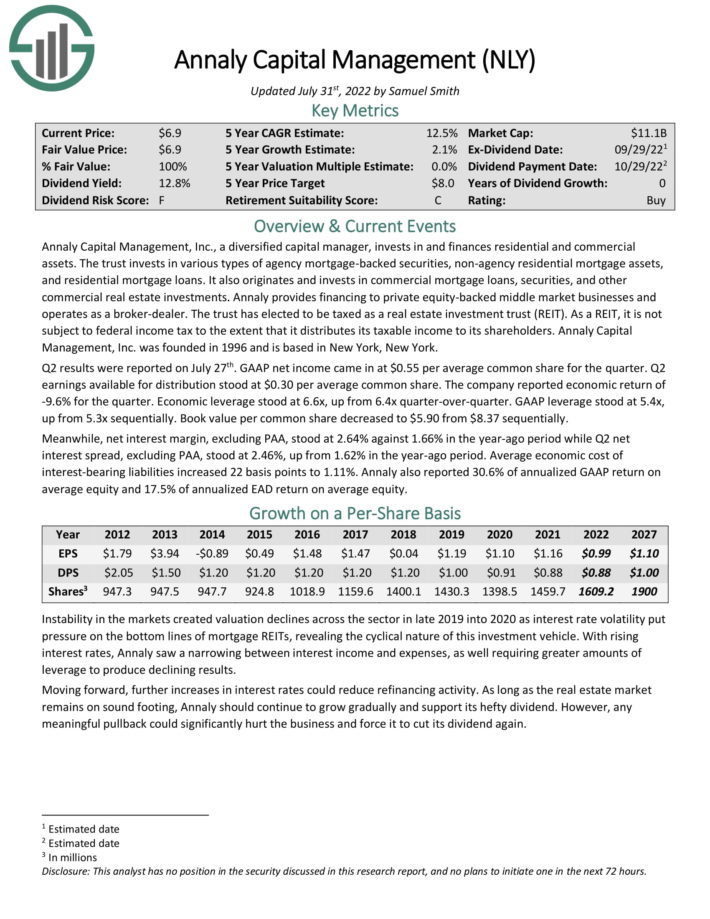

High-Yield REIT No. 3: Annally Capital Management (NLY)

- •Dividend Yield: 21.1%

Annaly Capital Management, Inc., a diversified capital manager, invests in and finances residential and commercial assets. The trust invests in various types of agency mortgage–backed securities, non–agency residential mortgage assets, and residential mortgage loans.

It also originates and invests in commercial mortgage loans, securities, and other commercial real estate investments. Annaly provides financing to private equity–backed middle market businesses and operates as a broker–dealer.

Source: Investor Presentation

Q2 results were reported on July 27th. GAAP net income came in at $0.55 per average common share for the quarter. Q2 earnings available for distribution stood at $0.30 per average common share. The company reported economic return of -9.6% for the quarter. Economic leverage stood at 6.6x, up from 6.4x quarter-over-quarter. GAAP leverage stood at 5.4x, up from 5.3x sequentially. Book value per common share decreased to $5.90 from $8.37 sequentially.

Meanwhile, net interest margin, excluding PAA, stood at 2.64% against 1.66% in the year-ago period while Q2 net interest spread, excluding PAA, stood at 2.46%, up from 1.62% in the year-ago period. Average economic cost of interest-bearing liabilities increased 22 basis points to 1.11%. Annaly also reported 30.6% of annualized GAAP return on average equity and 17.5% of annualized EAD return on average equity.

Click here to download our most recent Sure Analysis report on NLY (preview of page 1 of 3 shown below):

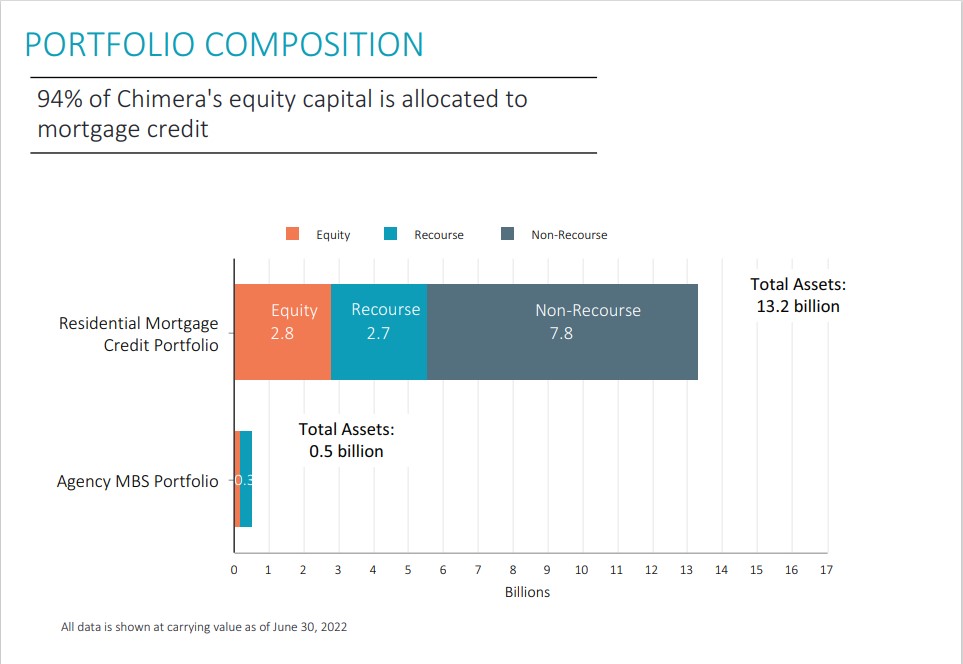

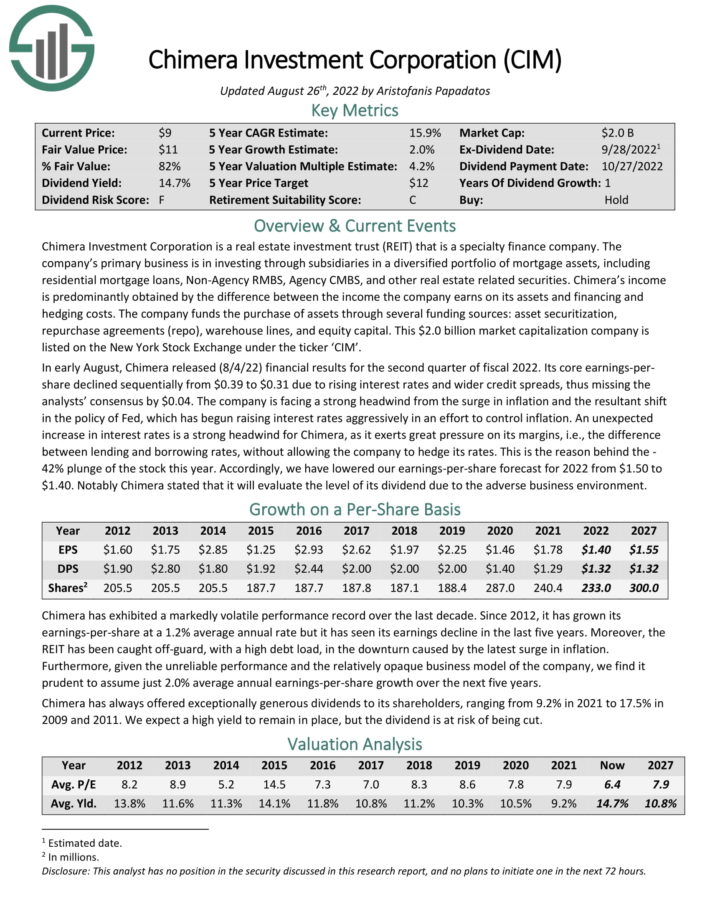

High-Yield REIT No. 2: Chimera Investment Corporation (CIM)

- •Dividend Yield: 24.1%

Chimera Investment Corporation is a real estate investment trust (REIT) that is a specialty finance company. The company’s primary business is in investing through subsidiaries in a diversified portfolio of mortgage assets, including residential mortgage loans, Non-Agency RMBS, Agency CMBS, and other real estate related securities.

Source: Investor Presentation

Chimera’s income is predominantly obtained by the difference between the income the company earns on its assets and financing and hedging costs. The company funds the purchase of assets through several funding sources: asset securitization, repurchase agreements (repo), warehouse lines, and equity capital.

Click here to download our most recent Sure Analysis report on CIM (preview of page 1 of 3 shown below):

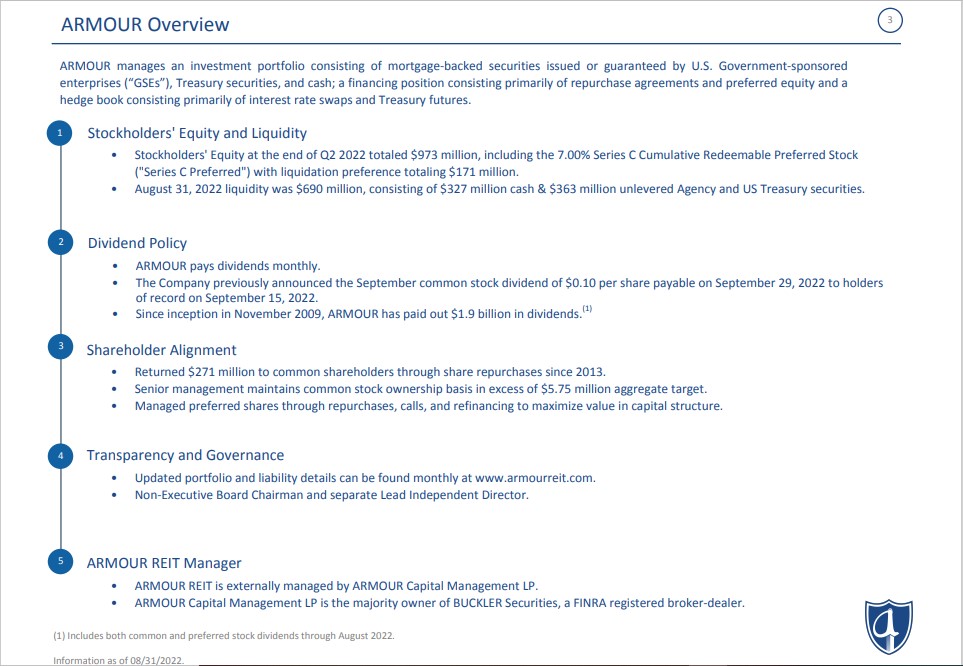

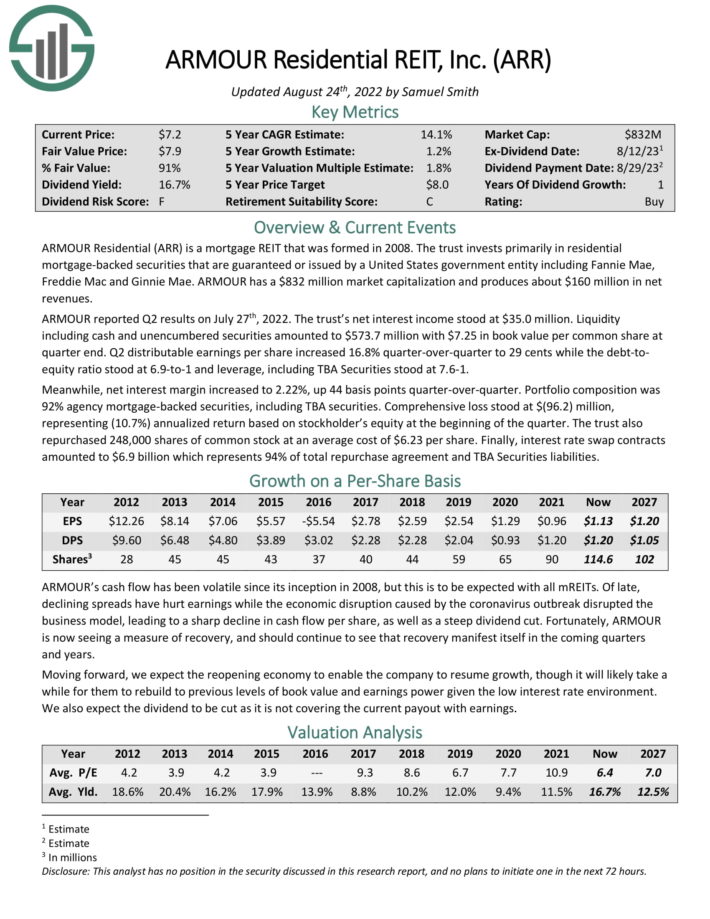

High-Yield REIT No. 1: ARMOUR Residential REIT (ARR)

- •Dividend Yield: 24.3%

ARMOUR is a mortgage REIT that invests primarily in residential mortgage–backed securities that are guaranteed or issued by a United Statesgovernment entity including Fannie Mae, Freddie Mac and Ginnie Mae. ARMOUR reported Q2 results on July 27th, 2022. The trust’s net interest income stood at $35.0 million.

Source: Investor Presentation

Liquidity including cash and unencumbered securities amounted to $573.7 million with $7.25 in book value per common share at quarter end. Q2 distributable earnings per share increased 16.8% quarter-over-quarter to 29 cents while the debt-to-equity ratio stood at 6.9-to-1 and leverage, including TBA Securities stood at 7.6-1.

Meanwhile, net interest margin increased to 2.22%, up 44 basis points quarter-over-quarter. Portfolio composition was 92% agency mortgage-backed securities, including TBA securities. Comprehensive loss stood at $(96.2) million, representing (10.7%) annualized return based on stockholder’s equity at the beginning of the quarter.

The trust also repurchased 248,000 shares of common stock at an average cost of $6.23 per share. Finally, interest rate swap contracts amounted to $6.9 billion which represents 94% of total repurchase agreement and TBA Securities liabilities.

Click here to download our most recent Sure Analysis report on ARR (preview of page 1 of 3 shown below):

Final Thoughts

REITs have significant appeal for income investors, due to their high yields. These 10 extreme high-yielding REITs are especially attractive on the surface, although investors should be aware that abnormally high yields are often accompanied by elevated risks.

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

This article was first published by Bob Ciura for Sure Dividend

Sure dividend helps individual investors build high-quality dividend growth portfolios for the long run. The goal is financial freedom through an investment portfolio that pays rising dividend income over time. To this end, Sure Dividend provides a great deal of free information.

Related: